Introduction

Many people experience a frustrating mystery at the end of every month when they look at their bank accounts. They work hard, receive their salary, pay their main bills, and expect to have money left over. Instead, they discover that their balance has dropped to almost nothing, and they cannot remember buying anything major.

This vanishing money is rarely caused by one big, expensive purchase. Instead, it happens because of small, hidden expenses that quietly drain your bank account every single day. These hidden expenses are called money leaks.

If you want to save money and stop feeling stressed before payday, you need to find these drains and plug them. This comprehensive guide serves as your ultimate Money Leak Analyzer: A Beginner’s Guide to Smarter Spending. By learning how to look at your daily choices, track your cash, and build a smarter spending guide, you can keep more of your hard-earned cash without giving up the things you love.

What Is a Money Leak Analyzer?

A money leak analyzer is not a complicated piece of software or something you need to pay an expert to use. It is simply a regular habit, a mindset, or a tracking system that helps you see small, automated, or impulsive expenses that take your money without making your life better.

Imagine your monthly income is like water pouring into a bucket. Your necessary bills like rent, groceries, and insurance are the official pipes where the water is supposed to go. Money leaks are tiny, unnoticed holes at the bottom of that bucket. Even if you pour a lot of water into the top, the bucket will eventually empty out if you do not patch those holes.

Using a clear method to check your cash flow gives you absolute clarity over your money management tips. It helps you change your habits from worrying about a zero balance to actively managing your cash. This practice can be useful for tracking and saving because it reveals the exact difference between what you think you spend and what you actually spend.

Why Money Leaks Happen

Money leaks do not happen because people are careless or bad with numbers. They happen because modern businesses make spending money too easy. With features like one-click online shopping, automatic renewals, and digital phone wallets, cash moves out of your account without you even noticing.

Understanding the main reasons behind these financial drains can help you protect your wallet. Here are the primary reasons why money leaks happen:

- Daily Untracked Expenses: Buying a quick snack, a morning coffee, or a short rideshare ride feels small at the moment. Because we rarely write down these minor costs, our brains pretend they did not happen, but they add up fast over thirty days.

- The Subscription Model: Many apps, streaming channels, and delivery services charge you automatically every month. Companies know that once you sign up for an auto-pay plan, you will likely forget to cancel it, even if you stop using the service.

- Easy Online Shopping: Online stores save your shipping address and payment details so you can buy items in two seconds. This removes the natural pause where you would normally think about whether you actually need the item.

- Lifestyle Inflation: When people earn more money, they naturally start spending more. They upgrade their plans, buy pricier groceries, or choose more expensive options without checking if the extra cost actually makes them happier.

- Small Convenience Fees: We often pay extra money to save a little bit of time. Extra delivery fees, app service charges, and out-of-network ATM fees seem tiny, but they quietly lower your savings over time.

Common Money Leaks and Fixes

To help you see how these daily habits affect your wallet, let us look at the most common money leaks beginners face, along with simple ways to fix them.

The table below shows common financial drains and how you can fix them easily.

Common Money Leaks and Fixes Table

| Money Leak | How It Affects Your Budget | Beginner-Friendly Fix |

| Unused subscriptions | Deducts money monthly | Cancel unused plans |

| Food delivery | Increases daily spending | Plan meals, set limits |

| Impulse shopping | Adds unnecessary expenses | Wait before buying |

| Credit card interest | Extra cost | Pay on time |

| Small daily purchases | Adds up over month | Track small expenses weekly |

| Lifestyle upgrades | Raises spending | Increase savings first |

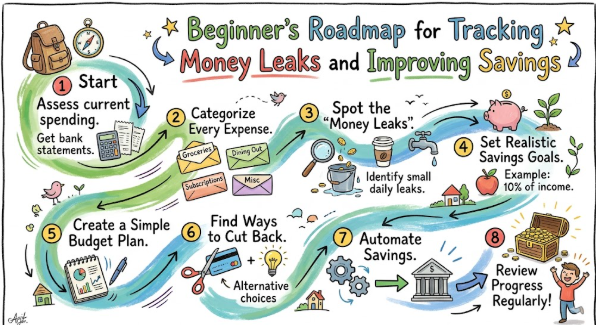

How a Money Leak Analyzer Works

Checking your daily finances for leaks does not require an accounting degree. All you need is a simple, step-by-step method to review your past accounts. Here is the basic system you can use to check your cash flow:

- Write Down Total Income: List the exact amount of money that enters your account each month after taxes. If your income changes from month to month, use a safe, lower average based on your past few months.

- Separate Fixed and Variable Costs: Group your bills into non-negotiable costs (like rent or car payments) and flexible costs (like eating out, clothes, or hobbies). Money leaks only happen in your flexible spending categories.

- Review Bank Statements Line by Line: Look at your bank accounts and card statements from the last 30 days. Check every single item. If you see a charge you forgot about or feel unhappy seeing, write it down as a leak.

- Group the True Leaks: Add up the total cost of your unused streaming channels, delivery service upgrades, or accidental free trials to see the exact amount of money you are losing each month.

- Set Clear Spending Limits: Once you see where your money is going, set simple weekly or monthly boundaries for those specific problem areas using personal finance tracking habits.

- Check Your Progress Every Month: Financial awareness is a continuous habit. Set a regular reminder at the end of every month to check your statements and make sure new leaks have not started.

Hidden Expenses Beginners Often Miss

When people begin learning about budgeting for beginners, they usually focus on large receipts like restaurant bills or new shoes. However, the real drains are often hidden inside small extra fees that we do not think about.

- Food Delivery Service Fees: A meal that costs a reasonable price at the restaurant counter can double in price on an app once you add delivery fees, service charges, and driver tips.

- Online Booking Charges: Buying event tickets, travel tickets, or movie seats online often comes with extra processing fees that add up over a year.

- Micro App Purchases: Spending a dollar or two a month for extra online storage, mobile games, or ad-free features seems harmless, but several small app costs together can upset your budget.

- Forgotten Free Trials: Signing up for a free one-week trial and forgetting to cancel it before the automatic billing starts is one of the quickest ways beginners lose money.

- ATM and Account Fees: Using a cash machine that belongs to a different bank or failing to keep a required minimum balance can trigger automatic fees that give you no value at all.

Psychology Behind Money Leaks

To know how to stop wasting money for good, we have to look at the feelings that make us spend. Spending money is rarely a purely logical choice; it is deeply connected to our emotions and daily stress levels.

- Stress and Coping Spending: After a difficult day at work or school, your brain wants a quick reward. Buying a new item or ordering comfort food gives you a temporary mood boost, acting as an emotional shield against stress.

- The Payday Feeling: When your paycheck arrives, you experience a natural feeling of wealth. This temporary confidence makes you drop your guard against impulse shopping during the first week of the month.

- Social Pressures and FOMO: Social media feeds showcase perfect vacations, trendy outfits, and expensive meals. This creates an internal pressure to match the lifestyle of your friends or online creators, even if it hurts your budget.

- The Search for Convenience: Modern life leaves people feeling tired. When your energy is low, it is easier to pay extra for a rideshare or order takeout instead of walking or cooking the food you already have at home.

Needs, Wants, and Waste: Smarter Spending Framework

Standard financial advice usually divides your money into two groups: Needs vs. Wants. However, to manage your money successfully, it helps to use a third category called Waste.

- Needs: These are the essential items you must pay for to live safely and maintain your job. They include your rent or mortgage, basic groceries, utilities, necessary medicine, and basic travel costs.

- Wants: These are expenses that make your life more enjoyable but are not required for survival. Examples include movie tickets, hobbies, fancy meals, or holiday trips. Wants are completely fine, as long as you plan for them intentionally.

- Waste: This is where money leaks live. Waste is money spent on things that bring you no happiness, no utility, and no long-term benefits. This includes gym memberships you do not use, late fees on bills, or clothes you buy but never wear.

Your main goal is not to stop spending money on your “Wants.” Instead, you want to get rid of “Waste” entirely so you have more cash available for your true goals and savings.

Step-by-Step Guide to Smarter Spending

Changing your financial routine into a smarter spending guide requires an easy, gradual approach. You do not need to change your entire life in one day; just follow these simple steps.

1. Log Every Transaction consistently

You cannot manage your cash if you do not know where it goes. Pick a simple tracking system that matches your lifestyle, such as a mobile app, a simple digital sheet, or a pocket notebook. Commit to writing down every single purchase.

2. Label Your Expenses Weekly

At the end of each week, look at your list of purchases and mark each one as a Need, a Want, or a Waste. Be completely honest with yourself during this review.

3. Cancel Wasteful Charges Right Away

The moment you spot an unnecessary expense—like an app you do not open anymore—cancel the account immediately. Do not wait for the next month or tell yourself you might use it later.

4. Save Your Money First

One of the most valuable money management tips is to automate your savings. Set your bank account to automatically move a small portion of your income into a savings account the day you get paid. This forces you to live on the money that remains.

5. Use the 24-Hour Delay Rule

When you want to buy something non-essential online or in a shop, force yourself to wait a full 24 hours before spending the money. This simple pause helps your logical mind decide if the item is a true want or just a quick impulse leak.

Real-Life Example: The True Cost of Micro-Transactions

Let us look at a realistic example involving a regular worker named Sarah. Sarah felt like she was living paycheck to paycheck, even though she earned a decent wage. She rarely bought luxury items, did not take expensive trips, and did not visit high-end restaurants.

When Sarah used a money leak analyzer to check her bank statements, she found out that small, daily choices were costing her a fortune:

- Daily Morning Coffee: Sarah spent $5.50 at a café near her office every workday morning. Monthly total: $110.

- Unused Streaming Accounts: She was paying for three video streaming sites but only watched one of them regularly. Monthly total: $30.

- Lunch App Delivery Fees: Instead of picking up her lunch from nearby sandwich shops, she ordered delivery three times a week, paying heavy extra fees. Monthly total: $144 in fees and tips alone.

- Forgotten Wellness App: A health app she downloaded for a New Year’s goal was still charging her account automatically. Monthly total: $14.99.

When Sarah added these small costs together, she realized she was losing nearly $300 every month on things she did not truly care about. Over a full year, that equaled $3,600—money that could have paid off her debts or built a strong safety net. This shows why answering where does my money go is much more important than just looking at large price tags.

Money Leak Analyzer Checklist

Use this basic checklist at the end of every month to keep your personal cash safe from hidden drains.

Money Leak Analyzer Checklist Table

| Checklist Point | Status |

| Monthly income reviewed | Yes/No |

| Fixed expenses listed | Yes/No |

| Daily spending tracked | Yes/No |

| Subscriptions checked | Yes/No |

| Credit card charges reviewed | Yes/No |

| Needs, wants, waste separated | Yes/No |

| Top money leaks identified | Yes/No |

| Weekly spending limit set | Yes/No |

| Savings transferred first | Yes/No |

| Monthly review completed | Yes/No |

Common Smarter Spending Mistakes Beginners Make

As you start practicing budgeting for beginners, try to avoid these common mistakes that can slow down your financial progress:

- Only Tracking Massive Purchases: Many beginners think their money is fine because they do not buy expensive electronics or designer clothes. Forgetting the tiny daily expenses is the main reason budgets fail.

- Trying to Be Perfect Instantly: Cutting out all fun spending immediately is hard to sustain. It causes frustration, which often leads to major impulse spending sprees later on.

- Leaving Auto-Pay Options Unchecked: Trusting your memory to cancel a free trial without setting an automated reminder usually leads to unwanted charges.

- Using Cards Like Free Cash: Spending on credit cards without tracking the running total can hide how much money you are actually spending, leading to surprise interest charges later.

- Ignoring Rare or Annual Bills: Yearly insurance costs, holiday gifts, or seasonal charges are not money leaks, but if you do not plan for them, they can ruin your monthly budget.

Practical Tips to Stop Money Leaks

If you want to plug your financial leaks right now, try adding these simple, helpful habits to your routine:

- Check Phone Subscriptions Weekly: Look directly at the subscription settings on your smartphone to find and cancel hidden automated app charges.

- Remove Saved Card Details from Websites: Make online shopping a bit harder by deleting your saved card numbers from internet browsers. Forcing yourself to get your physical card gives you time to change your mind.

- Prepare a Few Meals Ahead of Time: Cooking simple lunches or dinners at home reduces your reliance on expensive food delivery apps when you are tired after work.

- Switch to Annual Payments for Vital Services: For apps or tools you use every single day, check if paying for a full year at once is cheaper than paying month-by-month.

- Keep Your Spending Cash Separate: Transfer your weekly fun money to a completely separate account or card. Once that balance reaches zero, stop spending on entertainment until the next week.

How to Build a Smarter Spending Habit

Creating strong financial awareness takes time and patience. To make your money leak analysis stick for the long run, focus on making small, comfortable changes:

- Focus on Writing Expenses Down First: Do not worry about cutting your spending to zero immediately. Focus entirely on building the simple habit of tracking your purchases without feeling bad about them.

- Celebrate Minor Financial Wins: If you reduce your food delivery orders from four times a week down to two times a week, take pride in that choice. Small improvements build permanent wealth habits.

- Automate Your Bill Payments: Set up automatic payments for your critical utility bills so you never have to pay a late fee or extra interest charge again.

- Keep Your Financial Dreams in Sight: Whether you want to save for a car, a home deposit, or a life free of debt, keep a small reminder of your goal nearby to stay strong against impulse shopping.

When Should You Take Financial Help?

While using a money leak analyzer is an excellent way to clear up your finances, sometimes tracking tools are not enough. Personal finance tracking can be useful, but it cannot solve deeper financial problems on its own.

Consider speaking with a professional financial adviser or credit counselor if you find yourself in any of these situations:

- Your Necessary Bills Are Higher Than Your Income: Your absolute basic survival needs cost more than you earn, even after you cut out every single piece of waste.

- Your Debt Is Growing Out of Control: You are facing high-interest credit card debt or loan balances that keep growing despite your budgeting efforts.

- Money Causes Severe Stress: The simple act of looking at your bank account or thinking about your bills causes intense anxiety or panic.

- Your Income Is Highly Complicated: You manage complex freelance income streams, difficult tax situations, or business investments that need specialized advice.

Frequently Asked Questions

- What is the fastest way to find hidden money leaks in my accounts?

Look at your bank statements from the last 30 days and read through every line. Highlight any automatic renewals, app charges, or impulse shopping trips you forgot about.

- How often should I run a money leak analysis on my spending?

Reviewing your statements once a month is an excellent strategy for beginners. This helps you catch unwanted fees early and cancel services before you are charged again.

- Can I still enjoy dining out or shopping while fixing money leaks?

Yes, you can. Smarter spending is about removing waste, not eliminating joy. Budgeting helps you spend money on things you truly love while stopping payments on things that do not matter.

- Are digital budgeting apps safe for personal finance tracking?

Most popular budgeting apps use bank-level security to protect your information. If you prefer to keep things private, a spreadsheet or a regular notebook works just as well.

- What is the difference between a “want” and a “waste”?

A want is a planned expense that makes you happy, like a fun night out with friends. A waste is an expense that gives you no value, like paying for an app you do not open.

- How do I stop forgetting to cancel free trials?

The moment you sign up for a free trial, set an immediate reminder on your phone calendar for one day before the trial ends so you remember to cancel it.

- Does lifestyle inflation count as a money leak?

It can become a leak if it happens automatically without you noticing. Upgrading your lifestyle is fine as long as you balance it by growing your savings account first.

- How can I control emotional impulse shopping online?

Delete your saved payment details from your favorite shopping websites and internet browsers. Adding this extra step gives you time to think before you hit buy.

- Is it necessary to hire a professional to fix my spending habits?

Not usually. Most beginners can optimize their cash flow using free guides, basic tracking tools, and steady daily habits. Seek professional help if you are facing major debt issues.

- Will tracking small expenses like coffee really help me save?

Yes, it will, because small costs add up over months and years. Saving a few dollars a day might feel small now, but it can grow into a significant amount of money over time.

Conclusion

Discovering where your money goes does not require major personal sacrifices or an unhappy lifestyle. It just requires you to take a clear, honest look at your accounts so you can spot where your cash is slipping away. By using a basic tool like a money leak analyzer, you can easily guide your habits away from accidental waste and toward thoughtful, smarter spending.

Every dollar you protect by patching up a hidden financial drain is a dollar you can use to build an emergency fund, pay off debts, or save for your long-term dreams. Achieving true financial peace of mind depends on your choice to check your financial habits regularly and make small, steady adjustments over time.