Introduction

Reaching the end of the month only to find your bank account nearly empty is an incredibly frustrating experience, especially when you know you haven’t made any major luxury purchases. You paid your rent on time, cleared your utility bills, stuck to basic groceries, and yet your balance is still hovering dangerously close to zero. If this scenario feels all too familiar, please know that you are not failing at life—you are likely just dealing with invisible financial friction.

The reality is that most budgets do not fail because of big, deliberate splurges like a new couch or a weekend getaway. Instead, they are slowly drained by a continuous, unmonitored drip of everyday micro-transactions. In the world of personal finance, we call this hidden spending. Because these costs are individually tiny, they completely bypass your brain’s financial defense mechanisms. We don’t flag them as dangerous in the moment, but when dozens of these minor expenses compound over thirty days, they form massive money leaks that can completely derail your savings goals.

Learning how to spot and plug these invisible drains is one of the most powerful budgeting tips for beginners. By exposing exactly what these covert costs look like and understanding the psychological traps that let them slip through the cracks, you can learn to track expenses effectively and reclaim total control over your hard-earned money.

What Are Hidden Expenses?

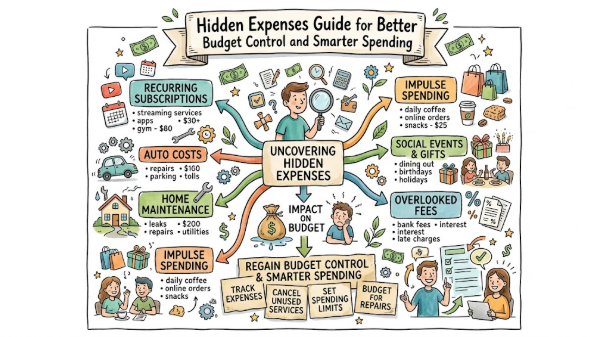

To master money management for beginners, you first need to understand the true nature of your financial adversary. Hidden expenses are not literally invisible; they appear clearly on your bank statements. Rather, they are “hidden” because they are structurally designed to bypass your active decision-making processes. Unlike fixed costs such as your rent or auto loan—which require large, conscious allocations of capital—hidden expenses operate quietly in the background of your daily life. They are often automated, disguised as small conveniences, or mixed into broader, everyday transactions.

Moreover, these costs subtly evolve alongside your lifestyle, income, and personal habits. For a student, a hidden expense might be the premium music streaming service they forgot to cancel after a free trial. For a salaried professional, it might be the compounding cost of midday gourmet coffees, premium delivery apps, or automatic cloud storage upgrades. Because these purchases are tiny in isolation, they do not trigger financial pain when they occur. Therefore, we fail to realize that a collection of small unnecessary expenses can easily equal or exceed the cost of a major monthly utility bill. Recognizing that these expenses exist is the crucial first step toward protecting your hard-earned cash.

Most Common Hidden Expenses Table

| Hidden Expense | How It Affects Your Budget | How to Manage |

| Subscription fees | Monthly deductions pass by unnoticed, locking you into passive payment cycles for apps, streaming services, or software you rarely use. | Review your bank statements, audit your active subscriptions quarterly, and completely cancel any unused services. |

| Delivery & convenience fees | Add small, incremental costs regularly to food, groceries, and retail orders, making each item significantly more expensive than its base price. | Plan your shopping trips ahead of time, batch your orders to clear minimum thresholds, and prioritize physical pickups when possible. |

| Micro-purchases | Daily coffees, snacks, and small items create a continuous, unmonitored leak that drains your liquid cash over the month. | Track your daily spending manually or via an app, and allocate a strict, finite cash allowance for casual daily indulgences. |

| Bank charges | Hidden fees, ATM maintenance charges, out-of-network costs, and transaction penalties quietly chip away at your account balance. | Monitor bank statements monthly, switch to zero-fee accounts, and strictly use in-network ATMs to avoid penalties. |

| Impulse buys | Spontaneous, unplanned purchases driven by clever marketing or emotional triggers ruin carefully planned monthly savings targets. | Implement a strict 24-hour waiting rule before finalizing any non-essential purchase to let your emotional impulse cool down. |

| Automatic upgrades | Automatic renewals, app upgrades, or unmonitored cloud storage tier increases scale your spending without your explicit consent. | Review your digital account settings regularly, turn off auto-renew by default, and audit application permissions. |

Why Hidden Expenses Sneak Into Budgets

It is important to remember that falling into overspending traps does not mean you are irresponsible with money. Modern payment ecosystems are intentionally engineered to make spending frictionless, which naturally invites money leaks into our daily routines. Let us break down the primary psychological and structural reasons why these hidden expenses manage to slip through the cracks:

- Untracked Micro-Transactions: Our brains are evolutionary wired to optimize for survival, not to calculate compound interest or track minor digital receipts. When you tap your card or phone for a tiny purchase, your brain does not perceive it as a threat to your financial security. Consequently, these micro-transactions bypass your internal mental ledger entirely.

- Forgetting Recurring Charges: The “subscription model” is highly profitable for corporations precisely because humans are naturally forgetful. Once you sign up for a free trial or an annual service, the payment shifts from an active decision to an automated behavior. If you are not actively auditing your accounts, these recurring charges will quietly repeat for months—or even years—without your awareness.

- Emotional Spending Habits: We frequently use small financial transactions as a quick mechanism to regulate our moods. For example, grabbing an expensive takeout meal after an exhausting workday or buying a minor retail item to celebrate good news feel like justified actions. However, when emotional comfort becomes tied directly to continuous spending, your budget bears the silent burden.

- Convenience-Based Spending: We live in an on-demand economy where time is highly valued. Premium apps charge convenience fees to save you minor effort, whether through grocery delivery, fast shipping, or skipping digital lines. While saving time is fantastic, relying constantly on convenience creates a premium lifestyle markup that drains your savings potential.

Step-by-Step Guide to Identify Hidden Expenses

1. Collect All Bank and Card Statements

Gather your financial documentation from the past three months. This includes checking account history, credit card portals, digital wallet transaction summaries, and payment app logs. Do not rely on memory alone, because your brain will naturally filter out small, inconvenient truths about where your money went.

2. Review Subscriptions and Recurring Payments

Go line-by-line through your statements specifically looking for repeating numbers. Highlight every recurring charge, no matter how small it appears. Pay close attention to memberships, streaming packages, cloud storage, premium software, app extensions, and fitness memberships. If you have not used a service within the last 30 days, it is a primary candidate for cancellation.

3. Track Small Daily Purchases

For the next 14 days, commit to writing down every single transaction you make, down to the exact cent. You can use a pocket notebook, a dedicated budgeting app, or a simple text file on your phone. Documenting the coffee, the vending machine snack, and the minor digital app download forces you to stay present and aware during the act of spending.

4. Categorize Spending Into Needs, Wants, and Waste

Analyze your gathered data and separate your expenses into three clear categories:

- Needs: Non-negotiable costs required for survival and baseline security (e.g., rent, basic groceries, utilities, minimum debt payments).

- Wants: Purchases that bring genuine joy or value to your life but are not strictly necessary (e.g., dining out with close friends, hobby supplies, entertainment).

- Waste: Fees, forgotten subscriptions, interest charges, convenience markups you didn’t need, and impulse buys that brought zero long-term value.

5. Analyze Spending Trends Over a Month

Calculate the total sum of your “Waste” category at the end of the month. Seeing this cumulative figure can be eye-opening. Rather than feeling guilty, use this empirical data as your baseline to adjust your habits for the upcoming month.

Real-Life Example: The Cost of Convenience

To understand how easily these minor items accumulate, let us look at a realistic scenario featuring a salaried professional named Sarah. Sarah earns a respectable income and adheres to a basic, informal budget. She pays her major bills on time and assumes that because she avoids luxury boutiques, her spending habits are completely optimized.

However, Sarah consistently wonders why she cannot manage to build an emergency fund. Let us take an honest look at what a typical month actually looks like for her behind the scenes:

Sarah’s Monthly Convenience Summary:

- The Daily Premium Coffee: Sarah stops by a local café every workday morning. At $5.50 per cup, across 20 working days, this adds up to $110.00.

- Food Delivery Convenience Fees: Exhausted after work, she orders dinner via delivery apps three times a week. Between service fees, delivery premiums, and delivery driver tips, she pays an average overhead markup of $12.00 per order. Across 12 orders a month, this equals $144.00.

- Forgotten Digital Subscriptions: Sarah maintains an active subscription to a premium video service she hasn’t watched in five months ($15.00), a productivity app she abandoned ($8.00), and a premium cloud storage tier she doesn’t actually fill ($4.00). Total cost: $27.00.

- Unnoticed Out-of-Network ATM Fees: To save time on weekends, she utilizes a convenience-store ATM near her apartment four times a month, incurring a $3.50 fee per transaction. Total cost: $14.00.

When Sarah adds these seemingly trivial items together, they total $295.00 every single month. Over the course of a calendar year, that amounts to $3,540.00 vanishing into administrative air. By simply modifying a few small daily routines—such as brewing coffee at home, picking up her takeout orders in person, and cleaning up her automated accounts—Sarah can redirect thousands of dollars toward her long-term savings goals without experiencing any structural drop in her overall quality of life.

Tips to Control Hidden Expenses

Once you have identified where your money is quietly leaking, you can begin deploying practical, proactive defenses. Use these foundational budgeting tips for beginners to create permanent barriers against lifestyle creep and invisible fees:

- Set Real-Time Spending Alerts: Access your mobile banking applications and enable immediate push notifications for every single transaction. Receiving an instant text or notification the second money leaves your account breaks the illusion of frictionless spending and forces you to stay aware of your balance.

- Utilize Dedicated Budgeting Apps: Move away from manual guesswork. Leverage modern personal finance tools to automatically aggregate your transactions, organize your accounts, and visually highlight when specific categories are approaching their limits.

- Cancel Unnecessary Subscriptions Immediately: If you discover a recurring service that you do not actively use, cancel it right away. Do not tell yourself you will “get around to it next week.” If you find you genuinely miss the service down the road, you can easily sign up again later.

- Embrace Strategic Meal Prepping: Food delivery apps are arguably the largest accelerators of modern budget damage. By planning your meals on Sunday, purchasing raw ingredients in bulk, and having home-cooked options ready in your refrigerator, you remove the decision fatigue that drives expensive last-minute delivery orders.

- Review Your Bank Statements Weekly: Do not wait until the end of the month to evaluate your financial performance. Dedicate 15 minutes every Sunday morning to review your account activity. This habit ensures you spot erroneous charges, unauthorized subscription increases, or accidental overspending before they escalate into major monthly issues.

Hidden Expense Tracking Checklist

| Checklist Point | Action Required / Notes |

| Subscriptions reviewed | Scan statements for any active recurring app or streaming charges. |

| Micro-purchases tracked | Log all cash, card, and digital payment snacks, coffees, and minor items. |

| Bank fees checked | Verify that no hidden maintenance or out-of-network ATM fees were charged. |

| Impulse spending monitored | Track any spur-of-the-moment purchases made throughout the week. |

| Automatic upgrades controlled | Audit app settings to ensure free trials haven’t converted to paid tiers. |

| Spending categories updated | Organize transactions accurately into your needs, wants, and waste logs. |

| Monthly review done | Sum up total spending across all accounts to assess overall performance. |

| Savings goals updated | Transfer recovered leak capital directly into your dedicated savings goals. |

| Alerts set for overspending | Confirm bank application push notifications are active for all accounts. |

| Budget adjustments applied | Refine category limits for the upcoming month based on historical data. |

Common Personal Finance Mistakes Beginners Make

When starting out on a wealth-building path, it is incredibly easy to fall into counterproductive mindsets. Recognizing these standard personal finance mistakes will help you avoid unnecessary guilt and keep you moving in the right direction:

- Ignoring Small Costs: The single most destructive belief is thinking, “It’s only five dollars, it doesn’t matter.” While an isolated five-dollar purchase is completely harmless, that same transaction repeated daily equals $150.00 a month. Every single dollar matters when it comes to the structural integrity of your broader budget.

- Failing to Track Daily Purchases: Relying entirely on automated monthly financial summaries at the end of the cycle is a reactive strategy. By the time you receive your end-of-month summary, the money is already gone. Proactive tracking requires monitoring things in real-time so you can pivot your behavior mid-month.

- Relying Solely on Mental Accounting: Assuming you can track your net worth, outstanding bills, and daily variable spending entirely in your head is a recipe for stress. Your mind is built for creative thinking and problem solving, not for storing rows of transactional financial data.

- Using Spending to Regulate Emotion: Treating shopping or premium convenience as an immediate cure for a stressful day is an unsustainable habit loop. It is essential to develop alternative, non-financial self-care routines—such as exercise, reading, or calling a friend—to decompress without draining your bank account.

- Neglecting Small Administrative Fees: Allowing banks to charge you monthly maintenance costs, account minimum penalties, or card fees simply because researching alternatives seems tedious is a clear example of unnecessary waste. Your financial institutions should be working for you, not quietly extracting your capital.

Practical Tips for Smarter Spending

Shifting toward long-term financial stability doesn’t mean adopting a mindset of painful deprivation. Rather, it means transforming into an intentional, conscious consumer.

Use this structured smart spending guide to maximize the tangible utility of every dollar you allocate:

- Track Every Single Currency Unit: Cultivate a healthy obsession with accuracy. Whether you utilize digital card transactions or physical cash, make sure every transaction is captured in your ecosystem. When you value your money enough to track it, you naturally treat it with higher respect.

- Set Highly Realistic Budgets: Do not design a perfect, hyper-restrictive budget that leaves zero room for fun or personal flexibility. If you completely restrict your personal spending category, you will inevitably experience budget burnout and abandon tracking altogether. Build a realistic plan that allows for occasional guilt-free treats.

- Ruthlessly Prioritize Needs Over Wants: Before finalizing any non-essential purchase, take a deep breath and ask yourself: “Do I need this item to function safely, or do I simply want this item right now?” This simple question creates a crucial cognitive pause that saves you from falling into common overspending traps.

- Automate Your Savings Goals First: Do not save what is left over after spending; instead, spend what is left over after saving. Set up an automatic transfer that routes a specific, manageable percentage of your paycheck directly into a separate savings or investment account the morning you get paid.

- Utilize Strategic App Reminders: Set up calendar events or app notifications two days before any major subscription auto-renews. This gives you an explicit window of time to evaluate whether that service still delivers authentic value before you are locked into another billing cycle.

Frequently Asked Questions (FAQs)

1. What counts as a hidden expense?

A hidden expense is any cost that slips past your daily awareness because it is automated, small in scale, or bundled into convenience charges. Examples include background application subscriptions, delivery markups, micro-purchases, and small bank administration fees.

2. How can I track micro-purchases effectively?

The most reliable method to track micro-purchases is to log them immediately using a mobile budgeting application or a dedicated text note on your phone right at the cash register. Documenting them in real time ensures they are never forgotten or overlooked.

3. Are digital subscriptions really a major problem for budgets?

Yes, because they are automated, recurring, and easy to forget. While an individual $10 service seems small, keeping multiple unmonitored subscriptions active can easily drain hundreds of dollars of your hard-earned income over a calendar year.

4. How often should I review my personal spending habits?

You should ideally review your transaction logs weekly to catch minor overspending early. Additionally, perform a comprehensive structural budget review at the end of every month to adjust your allocations and update your long-term savings goals.

5. Can budgeting apps genuinely help find hidden costs?

Absolutely. Modern personal finance applications automatically aggregate your historical transactions across multiple accounts, categorize your behaviors, and provide clean visual charts that highlight unexpected spikes in background spending.

6. How do I effectively cut down on premium convenience fees?

You can cut convenience fees by batching your online orders to hit free delivery thresholds, planning your grocery trips ahead of time, cooking meals at home, and prioritizing physical order pickup over home delivery services.

7. Do tiny daily expenses really add up over time?

Yes, they compound significantly. A minor $5 transaction repeated every single day adds up to $150 a month, which totals $1,800 across an entire year. Small leaks can absolutely sink a large financial ship if they go unpatched.

8. How do I permanently prevent emotional impulse purchases?

Implement a strict 24-hour waiting rule for any non-essential purchase. Removing yourself from the immediate retail environment or closing the digital shopping cart allows your emotional impulse to fade, enabling you to make a rational financial decision.

9. Should I track cash and credit card spending separately?

You should track them using separate categories inside your ecosystem, but ensure they are combined into your overall monthly budget review. Every single transaction matters equally, regardless of the underlying payment mechanism used to complete it.

10. When should I consider consulting a financial advisor?

Consider consulting a certified professional once you have successfully patched your basic hidden leaks, built a reliable emergency fund, and feel ready to navigate complex long-term wealth topics like tax planning, advanced investing, or retirement structuring.

Conclusion

Plugging the money leaks that are quietly draining your bank account does not require complex financial strategies or overnight lifestyle shifts. It simply requires turning your attention to the small details. Remember, true financial freedom is not built on a single, massive life event. Rather, it is achieved through the steady accumulation of small, intentional, everyday choices. By learning to track expenses effectively, auditing your subscriptions, and avoiding convenience-based overspending traps, you protect your hard-earned money and give every dollar a clear purpose.

Do not let invisible expenses dictate your financial future. Take immediate action today by choosing just two areas from our guide—like auditing your digital subscriptions or tracking your daily coffee purchases—and watch how much capital you naturally recover. Financial stability is a continuous journey, and you are entirely capable of steering it in the right direction.