Introduction

Many people find themselves wondering where their salary disappears by the end of each month, despite having covered all their major bills and essential costs; the reality is that personal financial instability is rarely caused by a single, catastrophic expense but is instead the result of a silent accumulation of trivial, day-to-day spending that goes completely unnoticed. These seemingly harmless habits—a morning coffee, a quick snack, or a forgotten app subscription—are often dismissed as inconsequential in the moment, yet when these micro-purchases are aggregated over weeks and months, they transform into significant financial drains that erode your ability to save and invest. Understanding how small daily purchases become big monthly losses is the fundamental first step in moving from a state of constant financial mystery to one of deliberate, intentional wealth building, allowing you to stop the erosion of your savings, close the “invisible” budget gap, and reclaim the financial freedom required to focus on your long-term goals instead of daily, unnecessary money leaks.

Key Consequences of Untracked Daily Purchases

- Erosion of Savings: Small, unplanned spending reduces the amount you can set aside for emergency funds or long-term investments.

- The “Invisible” Budget Gap: Without tracking, you cannot accurately identify why your monthly budget keeps failing.

- Reduced Purchasing Power: Constant micro-spending limits your ability to afford larger, more meaningful experiences or goals.

- Financial Stress: Even if you earn a good salary, the mystery of a dwindling bank account creates unnecessary mental fatigue and anxiety.

What It Is and Why It Matters

What it is:

Micro-purchases are those small, often unconscious daily expenses that slip through the cracks of your budget. Think of the $3–$5 coffee on your way to work, a spur-of-the-moment snack from the vending machine, recurring app subscriptions you rarely use, or those “just because” items at the checkout counter. They are rarely planned and often occur on autopilot.

Why it matters:

While a ₹100 or $3 purchase seems negligible, it is the frequency that matters. If you spend that amount every single day, you are losing thousands of rupees or dollars every year. This accumulation—often referred to as “death by a thousand cuts”—is the primary reason many people struggle to build wealth despite having a decent income. By identifying these leaks, you effectively give yourself a “raise” without having to work extra hours.

Why Small Purchases Add Up

The psychology behind small spending is subtle. Because these amounts don’t trigger the “pain of paying” that a large, one-time purchase does, we feel less guilty about spending them. However, when compounded, the effect is staggering.

- The Cumulative Effect: Small daily costs are mathematically significant when multiplied by 30 days.

- Repeated Habits: Much of our hidden spending is tied to routine. If you stop at a cafe every morning, you aren’t just buying coffee; you are building a habit that drains your wallet daily.

- Emotional Spending: Many micro-purchases are driven by small bursts of stress or boredom rather than actual need.

- Hidden Fees and Subscriptions: We often forget about “set-and-forget” subscriptions. A ₹150 monthly charge for an app you haven’t opened in months is a classic example of a money leak.

- Convenience Bias: We pay a premium for convenience—like food delivery fees or ready-to-eat meals—which adds a significant layer of expense over a full month.

Most Common Daily Purchases That Leak Money

| Daily Purchase | Average Cost | Monthly Impact |

| Coffee / beverages | ₹100/day | ₹3,000/month |

| Packaged snacks | ₹50/day | ₹1,500/month |

| Food delivery | ₹200/day | ₹6,000/month |

| Mobile apps / subscriptions | ₹150/month | ₹150/month |

| Impulse buys | ₹100/day | ₹3,000/month |

| Convenience items | ₹50/day | ₹1,500/month |

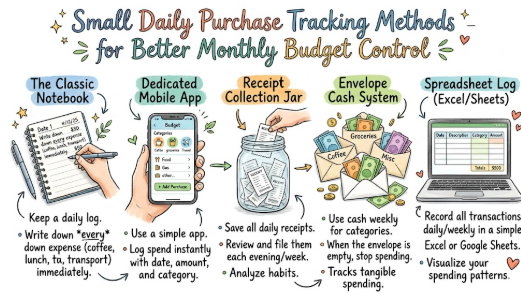

Step-by-Step Guide to Track Daily Spending

If you want to stop the leaks, you must first shine a light on them. Follow this systematic approach to master your daily expense tracking.

- Record All Daily Expenses: For one month, track every single penny spent. Use a notebook, a spreadsheet, or a dedicated budgeting app.

- Categorize Spending: Label every expense as a “Need” (rent, groceries), “Want” (subscriptions, eating out), or “Waste” (late fees, unused memberships).

- Calculate Totals: Aggregate these numbers weekly and monthly to visualize the total impact.

- Identify Recurring Micro-purchases: Pinpoint the automated or habitual expenses that repeat without your conscious decision.

- Review and Adjust: Use the data to set a “discretionary spending cap.” If you find you spend ₹3,000 on coffee, aim to cut that by half for the next month.

Real-Life Examples

- A professional buys a ₹120 coffee every workday, losing ₹2,880 monthly that could have been invested.

- A student orders daily snacks online, adding ₹1,500 to their monthly expenses without realizing the impact.

- A freelancer subscribes to multiple creative apps, paying ₹450/month for services they haven’t touched in months.

- A salaried employee buys lunch outside daily, spending ₹6,000/month instead of packing a simple, home-cooked meal.

- A couple repeatedly purchases small convenience items at the grocery store, totaling ₹3,000/month and reducing their savings goals.

Practical Tips to Reduce Hidden Daily Expenses

Small changes in habit lead to big changes in your bank balance. Here are some smart spending tips to help you keep more of your hard-earned money.

- Prepare at Home: Brew your coffee or pack snacks before leaving. It takes five minutes but saves thousands of rupees annually.

- Quarterly Subscription Audit: Every three months, review your bank statements and cancel any subscriptions you haven’t actively used.

- The “Wait 24 Hours” Rule: For any non-essential purchase, wait 24 hours before buying. Often, the urge to impulse-buy fades.

- Budgeting Apps: Utilize digital tools that categorize your spending automatically, so you can see exactly where your unnecessary expenses are hiding.

- Weekly Spending Limits: Carry a fixed amount of cash for the week for discretionary items. Once the cash is gone, the spending stops.

Daily Spending Tracking Checklist

| Checklist Point | Status |

| Daily purchases recorded | Yes/No |

| Weekly review of expenses | Yes/No |

| Categorization done | Yes/No |

| Subscriptions checked | Yes/No |

| Impulse purchases minimized | Yes/No |

| Savings impact calculated | Yes/No |

| Monthly total analyzed | Yes/No |

| Budget adjustments applied | Yes/No |

| Spending alerts set | Yes/No |

| Progress tracked regularly | Yes/No |

Common Mistakes Beginners Make

- Ignoring the “Small Stuff”: Believing that a small purchase doesn’t “count” toward the budget is the primary reason for failure.

- Skipping Daily Tracking: If you wait until the end of the month to record expenses, you will inevitably forget the small, cash-based purchases.

- Failing to Categorize: Simply listing expenses isn’t enough; you must categorize them to see which areas (e.g., eating out) are leaking the most money.

- Underestimating Recurring Payments: Many people forget about small, automated monthly fees that quietly erode their bank balance.

- Emotional Buying: Allowing moods—like stress or fatigue—to dictate your spending rather than your financial plan.

Frequently Asked Questions

- How do small daily purchases affect my budget?

They create a “death by a thousand cuts” scenario, where small, unnoticed expenses collectively consume a large percentage of your monthly income. - Should I track every single expense?

Yes, at least for the first 30–60 days. This creates the awareness needed to identify your specific spending patterns and leaks. - Can budgeting apps help track micro-spending?

Absolutely. Many apps sync with your bank accounts to categorize transactions automatically, making it easy to see where your money goes. - How often should I review my daily spending?

A weekly review is ideal. It’s short enough that you’ll remember why you made certain purchases, but long enough to see trends. - Are subscriptions really a problem?

They can be. Small, recurring payments for apps or services you don’t use are essentially money sitting idle that could be working for you elsewhere. - How can I reduce impulse purchases?

Implement the 24-hour rule: if you want something non-essential, force yourself to wait one full day. Most impulsive urges disappear by then. - Do small purchases really impact long-term savings?

Yes. The money spent on daily habits, if invested in index funds or savings accounts, could compound into a significant sum over a decade. - Should I include cash and card expenses separately?

Track both together. Your total budget doesn’t care if the money left your pocket as cash or digital currency; it’s all part of your total outflow. - How do I identify hidden recurring costs?

Review your last three months of bank statements specifically for monthly recurring charges (app stores, streaming services, memberships). - How can I set limits for daily spending?

Calculate your “wants” budget for the month, divide it by 30, and try to stick to that daily average.

Conclusion

Uncovering how small daily purchases become big monthly losses is a foundational step toward personal financial mastery. Remember, the goal of tracking your expenses is not to limit your joy or force you into a lifestyle of extreme frugality. Instead, it is about cultivating intentionality. By utilizing our structured daily expense tracking checklist, identifying your hidden spending leaks, and avoiding common personal finance mistakes, you reclaim absolute control over your financial future.

Every single small step you take today builds a stronger financial foundation for tomorrow. Take a close look at your spending habits this week, identify just one minor area where you can optimize, and watch how quickly those small savings transform into meaningful long-term financial security.